RATLINKS: TO INFINITY AND BEYOND

How AI Turned Every Weird Hobby Into a Scalable Business

In Niches There Are Riches

Alvin Murstein had it all figured out.

By 2013, the 71-year-old founder and CEO of Medallion Financial Corporation was sitting on top of one of the most profitable niche businesses in America. For three decades, Murstein had been lending money against small aluminum discs that cost $10 to produce in 1937 but were now worth $1.3 million each.

The New York taxi medallion represented the Platonic ideal of artificial scarcity economy, a carefully engineered shortage that would make De Beers jealous. Mayor Fiorello La Guardia capped the number of medallions at 13,237, a number that would remain unchanged for the next 77 years.

What followed was one of the most spectacular asset bubbles in American history, disguised as municipal transportation policy.

Murstein understood the beauty of artificial scarcity better than anyone. His company would lend against medallions at loan-to-value ratios that made mortgage brokers blush, sometimes financing 90% of a medallion's inflated value.

Why not?

The city had essentially created a protected market with limited competition. Medallions weren't just licenses to operate taxis; they were protected assets backed by regulatory barriers.

The math was intoxicating. A medallion that sold for $40,000 in 1980 was worth $200,000 by 1990, $400,000 by 2000, and over $1 million by 2010. Murstein's stock, whose ticker was TAXI, soared alongside medallion values, turning what should have been a mundane finance company into a Wall Street darling. Immigrant drivers mortgaged their entire futures against these metal tickets to middle-class prosperity, and banks like Medallion Financial happily facilitated the growth.

The ecosystem was perfect in its circularity: artificial scarcity drove up medallion values, which justified higher loans, which brought in more revenue for Medallion Financial, which made investors happy, which provided more capital to lend against medallions, which drove values higher still. It was a perpetual motion machine powered by regulatory protection and sustained by the assumption that this protected niche would continue indefinitely.

Murstein had every reason to believe the party would continue forever. After all, who was going to challenge a system that had survived the Great Depression, World War II, the social upheavals of the 1960s, the fiscal crisis of the 1970s, and the tech boom of the 1990s?

Then, in May, 2010, a black sedan pulled up to a San Francisco street corner. The passenger didn't hail it, didn't call dispatch, didn't fumble for cash. They simply opened an app called UberCab and tapped a button.

THE GREAT MEDALLION MELTDOWN

Within five years, those million-dollar medallions had cratered to $120,000. TAXI stock, which had peaked above $20 per share, collapsed to under $3. The carefully constructed scarcity that had supported an entire ecosystem evaporated overnight. Not gradually, not with warning signs, but with the brutal efficiency of a guillotine. Suddenly, everyone with a smartphone and a 2007 Honda Civic could become a taxi.

The medallion collapse wasn't just about ride-sharing. It revealed something fundamental about how technological disruption works. When new technology democratizes access to previously protected markets, the old gatekeepers don't gradually lose power; instead, they become instantly irrelevant.

The same forces that destroyed Murstein's empire contain the seeds of something more profound. The technology that eliminated artificial scarcity didn't just tear down barriers; it created infinite new possibilities for those willing to see them. What emerged from the wreckage of the medallion system wasn't chaos, but a new kind of economic order where individuals could build profitable businesses in markets too small for traditional companies to even recognize.

The question isn't whether protected niches will survive. They won't. The question is whether you'll be among those who learn to create new ones faster than the old ones disappear.

BACK TO THE FUTURE

The future arrived for me on a Tuesday afternoon while complaining about my local sushi restaurant's missed merchandising opportunity.

Fujihana represents a peculiar modern paradox: a restaurant whose logo vastly outperforms its food. The design is clean, distinctive, and memorable. Exactly the kind of mark that would look perfect embroidered on a hat. Yet they sell no merchandise, despite operating in a city where restaurant merch has become its own category of social currency.

After the standard “someone should do something about this” conversation with a friend over our salmon rolls, I found myself saying something that surprised even me: “You know you can just make things now, right?” The words hung there between the wasabi and the soy sauce, a revelation disguised as small talk. My friend nodded, assuming I was having another one of my theoretical business epiphanies. But this time was different. This time I meant it.

Total time invested: twenty minutes.

Total cost beyond the hat itself: zero dollars.

Six months ago, this impulse would have died the typical death of Tuesday afternoon inspiration. Buried under the weight of minimum order quantities, setup fees, and the thousand other frictions that separate ideas from reality. Today, it represents something more profound: the complete collapse of the distance between conception and creation.

This transformation reveals the inverse of Murstein's medallion economy. Where his world was built on artificial scarcity (13,237 medallions and not one more), the new economy operates on artificial abundance. Infinite shelf space, zero marginal costs, and production systems that respond to individual demand rather than mass market projections.

The medallion holders spent decades competing for access to a fixed, protected market.

The taxi empire collapsed when technology eliminated the barriers that made the business model possible. But that same technological force didn't just destroy, it created new possibilities for value creation at scales previously unimaginable.

The difference between then and now? Instead of needing city hall to protect your market, you can create markets that protect themselves through their very specificity. The narrower the niche, the wider the moat.

Today's opportunity lies in creating markets that didn't exist yesterday, or serving needs so specific that traditional businesses can't economically address them.

Understanding this shift requires examining how we got here. A transformation that began twenty years ago, when a business writer noticed something peculiar happening in the entertainment industry.

THE LONG TAIL MEETS THE INFINITE LOOP

In 2004, Wired editor Chris Anderson published "The Long Tail," arguing that infinite shelf space would make niche products economically viable. What he couldn't have predicted was how AI would collapse production costs so completely that the long tail would become the whole dog.

Anderson's progression of predictions reads like economic prophecy:

"The Long Tail" showed how digital distribution made niche markets profitable

"Free" demonstrated how marginal costs approaching zero created new business models

"Makers" revealed how democratized production would transform physical goods

We're now living in the convergence of all three predictions, turbocharged by AI. We have infinite shelf space (Long Tail), near-zero distribution costs (Free), and democratized production tools (Makers). But AI serves as the catalyst that makes all three economically accessible to individuals, not just corporations.

The original long tail required significant investment to serve small markets. We're now living in the convergence of all three predictions. Serving a tiny, passionate market costs almost nothing and often outperforms mass market attempts.

The new economic framework is elegantly brutal in its simplicity:

Identify categories with weak or non-existent leaders

Build superior products in days, not months

Optimize for specific audiences, not mass markets

Capture value before competitors even notice the opportunity exists

This theory proved compelling in academic circles, but I didn't understand its practical implications until I started receiving the same feedback repeatedly across different projects.

WE’RE TALKING ABOUT PRACTICE

Feedback lurks everywhere, whether you want to hear it or not.

Opinions are like assholes, everyone has one.

When I launched Peel and Eat: A Gentleman's Guide to Gambling on Golf, the most common response wasn't about the content.

It was a question: “Can you make an app?”

I pushed back, explaining that many exclusive clubs where high-stakes wagering occurs don't even allow cell phones on the premises, let alone on the course. That's exactly why I created a book with tear-out scorecards.

After the fourth person asked about an app, the feedback finally registered.

I made the app, it’s a mobile-first golf system for 8 golf gambling games.

Sometimes the market knows something you don't, even when you're positive you know better.

A few years ago, turning a concept into an app would have meant hiring developers, learning to code, or accepting that the idea would remain just that: an idea. When the book launched in May, I attempted to vibecode the Peel and Eat app. I got remarkably far before hitting the inevitable wall where ambition exceeded ability. The app was functional but not great, and I yearned for greatness.

This month, I tried again and built an app in an afternoon. Still not great, but a marketable improvement.

The improvement curve follows what economists call a J-curve: initial slow progress followed by explosive acceleration. We went from "AI can help with coding" to "AI can build entire applications" to "wait, why do I need to think about code at all?"

HEROES ON THE HALF SHELL

Turtles all the way down comes from an old cosmological joke about infinite regress. A scientist explains that Earth rests on a giant turtle. When asked what the turtle stands on, the answer is another turtle. And that one? Another turtle. It's turtles all the way down.

In the AI economy, this infinite regress became a feature, not a bug. Each layer of automation creates the foundation for the next layer of creation. AI helps you build tools that help you build better tools that help you build businesses that help you build entire ecosystems. Every turtle supports a new universe of possibilities.

I had seen this pattern before.

In July 2023, working with two talented CTOs, we built reheat.ai, the world's first infinite cookbook, in just a few weeks. We faced a fundamental startup dilemma: marketing drove traffic that increased our costs faster than our revenue. Classic venture math suggested we needed to grow users first, monetize second. Instead, because of the feature set offered through our AI, we attempted to sell the company to a bigger player who could afford to grow the user base.

We got very close to selling Reheat.ai to two different major consumer food conglomerates. Unfortunately, large corporations move at a glacial pace. Meanwhile, OpenAI launched ChatGPT, allowing people to simply prompt for recipes, making our "infinite cookbook" feel less special.

We fell into the cruelest trap of the new economy. The gap between building something novel and building something necessary. We had a solution in search of a problem, and by the time we found the problem, the solution had been commoditized.

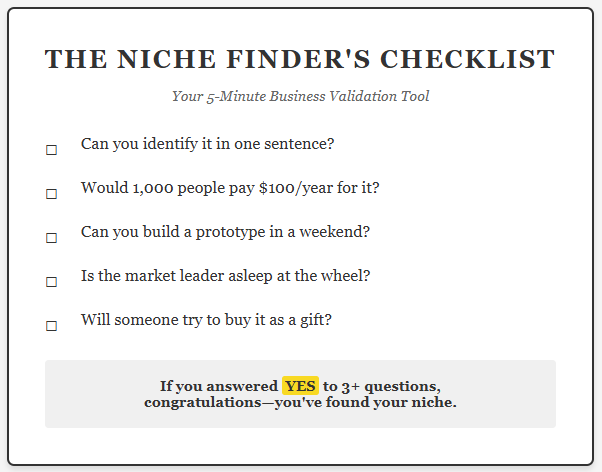

THE GIFT TEST

The cost of failure is just tuition if you're paying attention.

What I learned from Reheat's demise would prove invaluable: product-market fit isn't a theory. It's that moment when someone tries to buy something you just made as a gift.

After creating my Fujihana hat, I developed a Grateful Dead Dancing Bear-branded hat for my local golf club. I brought one to the starter as a gift. As I was leaving, another employee approached me and tried to purchase the hat for $50.

That's product-market fit. Not surveys, not focus groups, not elaborate market analysis. Just someone willing to pay real money, right now, for something they didn't know existed five minutes ago. He ordered four hats on the spot. Later that night, the starter called to order five more after his daughter had stolen his.

This validation opened the floodgates.

Could vintage art prints follow the same pattern as the hats?

I quickly created a faux-vintage line called The Turnberry Open, modeled after a real golf tournament, but I wondered: what would happen if I gave AI free rein to create sixty years of alternative tournament history? Within one afternoon, I was looking at vintage posters for each year, all rendered in period-perfect detail.

See the opportunity. Create the product. Test the market. All before lunch.

When you can create and test products in hours instead of months, the entire calculus of business changes.

You don't need to be right the first time. You need to be fast enough to be wrong twenty times before your competitor is right once.

Two years ago this month, Ratlinks described the AI application layer. It's worth revisiting if you're interested in the mechanics of why some AI applications thrive while others become footnotes.

GAMING THE SYSTEM

Before creating any product or launching any venture, you need to think like a customer, not a creator.

Work backwards from desire, not forwards from capability. This seems obvious until you realize how many billions have been burned by people who did exactly the opposite.

A few years ago, I launched CalinY, a streetwear brand for the urban cowboy. Our featured product was the Urbolo, an interchangeable bolo tie. We got featured in Businessweek, which felt like validation, but fashion is fickle, and trends move faster than supply chains.

Individual validation only scales if you pick the right market.

Peel and Eat further proved this when last month Golf Digest featured my book in an article about how to play “Bloodsome.” The article drove sales and launched the book into Amazon's top 50 gambling books. A category I didn't even know existed until I was competing in it.

Suddenly, I was wondering: how do I become number one on this list?

That's when I noticed something beautifully absurd about Amazon's rankings. The gambling books category is consistently dominated by ... Yahtzee scorecards. Not poker strategy guides. Not blackjack systems. Not sports betting analytics. Yahtzee scorecards.

This isn't because America is experiencing a Yahtzee renaissance. It's because scorecards represent the perfect storm of niche economics: consistent demand, zero complexity, infinite variations, and a market too small for major publishers to care about but too profitable for smart operators to ignore.

Last week, this observation crystallized into GameMaster. A systematized approach to the scorecard economy. It's not revolutionary. It's not disruptive. It's not going to be featured in TechCrunch.

It's just a profitable print-on-demand publishing business focused on premium game scoresheets, targeting top rankings in multiple Amazon categories by doing what incumbents don't. Caring about design and teaching game-winning strategies.

The initial portfolio contains Yahtzee, Bunco, Farkle, Phase 10, and Mexican Train scorecards. Each is designed to be slightly better than existing options, priced slightly higher than commodity alternatives, and marketed to rank on the first page of search results.

You can do it too. Find an underserved category, build a superior product, capture market share. Repeat across multiple categories.

THE CATEGORY CREATION REVOLUTION

We're witnessing the third great wave of economic transformation in modern history. The Industrial Revolution created entirely new job categories: factory workers, railroad engineers, quality control specialists. The Internet Revolution birthed digital natives: web developers, social media managers, data scientists.

Now the AI Revolution is generating its own wave of category creation. The obvious ones are already emerging: AI prompt engineers, synthetic media specialists, algorithm auditors, vibe coders.

These jobs represent just the visible surface. The real transformation is happening at the micro level, where thousands of new categories are being born daily. Categories too specific to be jobs, too niche to be industries, but profitable enough to be businesses.

The deeper transformation is happening at the micro level. Every displaced worker isn't just a potential category creator. They're entering an economy where thousands of new micro-categories are being born daily. Categories so specific and niche that they couldn't support a business before AI made serving them economically viable.

Custom study guides for homeschoolers with dyslexic children learning Mandarin

Meal plans for people with both FODMAP sensitivities and cultural dietary restrictions

Sleep music generated specifically for your unique brainwave patterns

Exercise routines for people who exclusively work out during commercial breaks

When you can serve a market of 1,000 people profitably, you don't need to chase millions.

FROM SCARCITY TO INFINITY

The medallion economy operated on a simple principle: control access to artificially scarce resources, then extract rent from those who need them. Murstein's fortune came from the city's declaration that only 13,237 medallions could exist. No more, no less, forever and ever, amen.

When technology erased that constraint, his empire didn't gradually decline. It vaporized. But technology didn't just destroy artificial scarcity. It created infinite real abundance. Where Murstein fought for access to one protected market, we can now create unlimited markets. Each is perfectly sized for its audience, each too small for traditional companies to bother with, each profitable enough to matter.

The medallion holders spent 80 years protecting their artificial scarcity, only to watch it evaporate in 80 months. In their place stands something far more valuable: the ability to create value where none existed before, to serve needs too specific for mass markets, to build businesses that grow with their communities rather than despite them.

Murstein's mistake wasn't his business model. It was believing that barriers create value. In the AI economy, the only sustainable barrier is being first to profitably serve a need nobody else has noticed.

The old economy was about competing for a fixed pie. The new economy is about baking infinite pies, each one a potential category you can own.

Today's opportunity isn't in protecting what you have, it's in creating what doesn't exist yet.

In a world where anyone can make anything, the only real scarcity is the ability to notice what should exist but doesn't. That's not a skill you can regulate, monopolize, or lobby into existence. It's just the practiced art of paying attention.

In niches there are riches. The question isn't whether you can find a niche. The question is how many niches you can create.

What are you going to build today?